Singapore's dynamic real estate landscape presents a compelling problem for investors and businesses: to own or to lease commercial property? Each path unlocks a unique set of potential rewards and risks, demanding careful analysis before diving into the market. Navigating this nuanced decision requires a deep understanding of the financial considerations, market trends, and strategic implications of ownership and leasing.

Understanding Real Estate Ownership and Commercial Leasing

Real estate ownership involves acquiring property outright through personal funds or financing. Owners reap the rewards of any appreciation in property value and can generate income through renting out the space.

On the other hand, commercial leasing involves renting a property from an owner for business purposes. Lessees enjoy the use of the property without the hefty initial capital outlay of ownership, offering greater flexibility and potential cost savings. Commercial properties are usually comprised of the following property types:

- Industrial

- Retail

- Office

- Shophouse

- Mixed Development

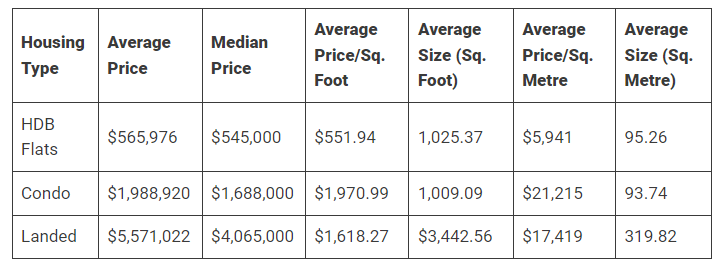

The real estate market in Singapore is a unique blend of public and private housing options. The public sector is dominated by HDB flats, which are government-subsidized residential units designed to be affordable for most Singaporeans.

Conversely, the private sector comprises condominiums and landed properties, typically carrying heftier price tags but offering enhanced amenities. Over the years, Singapore's property market has demonstrated relative stability, with property values appreciating consistently.

Since 2008, residential properties have been the preferred choice for property investment until the recent implementation of MAS cooling measures. These measures include loan restrictions, rising prices, and an additional buyer’s stamp duty (ABSD), making securing capital for purchasing a second property more challenging.

Commercial properties have emerged as an appealing alternative with the increasing regulations and costs associated with residential properties. This is primarily because commercial properties remain unaffected by the cooling measures due to reduced speculative activity.

Commercial properties usually cost less per square foot, primarily because of shorter leases lasting only 30-60 years. While freehold commercial properties exist, they are rarely found in prime business areas.

The prices of commercial properties tend to be more volatile as their value is closely tied to the industry outlook. For instance, if semiconductor manufacturers occupy the property, one must closely monitor industry exports. In an industry slowdown, tenants may need to shut down or relocate to more affordable locations.

Here’s a more detailed breakdown:

Private Property Costs:

- Option Fee (OTP): 1-10% of the sales price to secure the property; forfeited if the buyer backs out.

- Down Payment: Difference between purchase price and loan granted.

- E.g., For a $1 million property with an 80% loan ($800,000):

- Option fee: 1% = $10,000

- Option exercise fee: 9% = $90,000

- Down payment: $200,000 less option monies = $100,000

- At least 5% of the down payment must be cash; the remainder can be cash or CPF.

Stamp Duty on Purchase Price:

- Buyer's Stamp Duty (BSD): Tax paid once OTP is signed, with rates varying by property price:

- First $180,000: 1%

- Next $180,000: 2%

- Next $640,000: 3%

- The remaining amount is 4% for residential properties and 3% for non-residential properties.

Additional Buyer’s Stamp Duty (ABSD):

- Applies to second property purchases by Singaporeans, PRs, and foreigners.

- Rates vary from 0% for first-time Singaporean buyers to 20% for foreigners.

- Stamp Duty on Mortgage Documents: 0.4% of the mortgage amount, capped at $500.

Legal Fees: Approximately $2,500-$3,000 via bank-appointed lawyers; variable for private lawyers.

Valuation Fee: Between $350 and $500, sometimes covered by the bank.

HDB Flat Costs:

- Option Fee: $1 to $1,000.

- Option Exercise Fee: Up to $5,000, including the option fee.

- Down Payment: 10% of the purchase price.

- Valuation Fee: $140 to $200.

- Resale Application Fees: $40 to $80.

- Legal Fees: Variable; refer to the HDB website.

- Insurance: Fire insurance is mandatory for HDB loan borrowers, costing $1.50 to $7.50 for a five-year term.

Administrative Fees:

- For HDB flat application: $10.

- For temporary extension of stay: $20.

- Buyer’s Agent Fees: Usually 1% of the purchase price for HDB flats.

Additional Costs: Buyers may also need to cover pro-rated property tax or utility bills paid in advance by the seller.

For detailed rates and conditions, especially for stamp duties, it is recommended to check the IRAS website. Legal fees, stamp duty, and valuation fees can typically be paid using either cash or CPF savings.

Commercial properties generally offer higher returns over a 5 to 10-year period than residential properties. However, considering rental yields instead of capital gains can also prove advantageous when viewing a commercial property as a long-term investment.

The rental yields for residential properties range from 2% to 3%, while commercial properties can yield almost double that, averaging around 5%. However, unlike residential properties, commercial properties require ongoing asset enhancement.

Renting out an unfurnished 3-room condominium is much easier than a bare office. If you can tailor your property to suit the needs of potential tenants, your chances of increasing your capital outlay will rise. Of course, you may have to accept a lower rental yield if you are particular about your tenants.

Understanding Capex in Real Estate

Capital Expenditure, or capex, is a vital concept in general business and the real estate market. So, what is capex? It’s the funds used to acquire or upgrade physical assets such as land, equipment, or buildings. This type of expenditure is crucial for businesses looking for long-term benefits.

For example, this might include purchasing a property or significant renovations in real estate. It's different from operating expenses (opex), which are the day-to-day expenses needed to run a business, like payroll and utilities. While opex is recorded on the profit or loss statement, capex is capitalized on the balance sheet under assets, and as these assets are used, they are depreciated.

In the competitive Singapore real estate market, landlords often finance capex to make properties more appealing and lease them out faster. This is especially true for high-end or commercial properties requiring specific tenant modifications. Landlords might recover these costs by increasing base rental, amortizing costs over the lease term, or requiring higher security deposits to mitigate risk.

Capital expenditures are broadly categorized into maintenance capex and growth capex. Maintenance capex is about replacing assets to maintain current operations and revenue levels, like swapping out an old forklift in a warehouse. Growth capex, however, focuses on expanding business potential, such as buying additional forklifts for a new warehouse to increase capacity.

In summary, understanding the difference between capex and opex and the strategic use of capital expenditure in sectors like real estate is key to long-term business growth and sustainability. Whether it’s for maintaining current operations or expanding into new markets, capex represents a significant and necessary investment in the future of a business.

What To Expect With Owning a Commercial Real Estate

While purchasing a commercial property offers exciting opportunities, it comes with distinct differences compared to residential properties. Here are several vital points to consider:

- Financing: You cannot use your CPF for commercial properties. Additionally, banks have different lending policies for each type, with stricter LTV ratios (60% – 70%) than residential (70% – 80%). Loan tenures are shorter (20 – 30 years vs. up to 35 years), and interest rates are typically 0.5% – 1% higher.

- Taxes: Commercial properties are exempt from Additional Buyer Stamp Duty (ABSD), but some, like industrial properties, have a Seller’s Stamp Duty (SSD) based on a holding period (15% within one year, decreasing to 5% by year 3). Property tax is flat at 10%, compared to the residential variable rate depending on occupancy (0% – 15% owner-occupied, 10% – 20% not).

- Occupancy: Purchasing for owner-occupancy can unlock a 10% higher loan amount than pure investment.

- GST: Purchases from GST-registered companies incur a 7% GST, but you can claim it back if your company is GST-registered.

Purchasing a commercial property involves various financial considerations based on the property type. The economic climate also influences the property's price. A flourishing sector leads to increased tenant demand and rental rates, while a recession can have the opposite effect, reducing rental yields.

A 9% Goods and Services Tax (GST) is also applicable when buying commercial real estate. CPF funds or bank loans cannot cover this tax, necessitating sufficient cash reserves to handle this expense. It's important to note that GST applies to movable furniture and fittings within these properties.

Regarding furniture, outfitting commercial spaces such as offices with furnishings can enhance their rental value. However, this means additional expenditure on items like tables and chairs. Importantly, attempting to reduce costs by importing inexpensive furniture from platforms like Taobao or AliExpress won't bypass GST, as all imports valued at $400 or less are also subjected to this 9% charge.

Renovation is another factor to consider, similar to residential properties. This is particularly relevant when purchasing a more affordable, potentially run-down commercial property that would require refurbishing. Renovation, on average, can cost you between $70 - $150 per square foot, depending on layout complexity, flooring, size of electrical furnishing, and more.

Weighing the Options: A Framework for Decision-Making:

Navigating Singapore's dynamic real estate market requires a custom-fitted decision, not a one-size-fits-all approach. Only some people possess the hefty capital for ownership; even those with the means might prioritize higher ROI growth ventures for their businesses. Ownership's allure lies in long-term appreciation and control. Still, it demands a significant upfront investment and a risk-tolerant stomach—leasing, on the other hand, beckons with flexibility, lower costs, and mitigated risks.

Ultimately, the key lies in a tailored approach. Weigh your investment horizon, risk tolerance, resources, and business objectives against each option's advantages and disadvantages. Conduct thorough due diligence, seek expert guidance, and align your choice with your needs and aspirations. In this diverse market, informed decisions pave the way for immediate and long-term success.

Singapore's commercial real estate market is constantly evolving, driven by technological advancements, changing consumer preferences, and evolving government policies. The rise of coworking spaces and the growing demand for flexible work arrangements are reshaping the landscape, presenting opportunities and challenges for ownership and leasing strategies. Understanding these trends and anticipating future scenarios is crucial for making informed long-term investment decisions.

Comments (0)

Subscribe via e-mail